Grantor Retained Trust

You setup or amend your living trust when the plan is to reduce estate taxes while giving assets to family members. The idea is to freeze the value of your estate below the $11,400,00 limit. Let the next generation get the upside appreciation. This is a “future” interest gift.

What you do is create and fund the trust with assets you expect to appreciate over time. Meanwhile, you can get income from the assets for a period of years.

The upside appreciation is now outside of your taxable estate. If you’re up against the lifetime limit, it would avoid gift tax on the excess amount.

The difference in the types of trusts are in their method of determining income payments. These trusts are irrevocable, meaning you cannot reverse or undo them. Otherwise you lose the tax benefits.

You report any income on your personal tax return. This is how ‘grantor’ trusts, per IRS rules, are taxed.

Grantor Retained Income Trust

You transfer assets to the GRIT while retaining the right to receive all net income until death or a fixed term of years. Your trustee distributes the income annually or more frequently as determined by the trust agreement.

If you live past the fixed term period, any remaining principal is either distributed or held for your heirs. And if you survive the initial term of the trust, the principal is excluded from your estate for federal estate tax purposes.

Your initial gift to the trust is discounted for federal gift tax purposes. The amount depends upon the term of the trust, and the applicable federal rate in effect in the month that the GRIT is established.

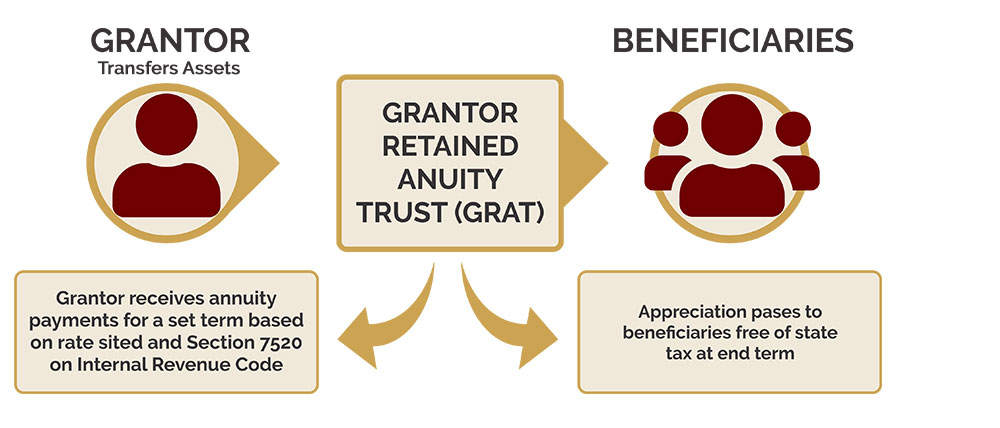

Grantor Retained Annuity Trust

These are similar to GRITs except that your income is a specific amount or fixed percentage of the value of the assets transferred to the trust. Your initial gift gets a valuation discount for tax purposes.

When the trust term expires, you no longer receive any income from the trust. The assets are transferred to your heirs. If you survive this term, the remaining principal (to heirs) is excluded from your estate for federal tax purposes.

In other words, the transfer of property to a GRAT constitutes a gift equal to the total value of the property transferred to the GRAT, less the present value of the retained annuity interest held by the Grantor.

The story is that Mark Zuckerberg used this trust for his Facebook stock before the IPO.

Grantor Retained Unitrust

This is similar to a GRAT except that your income is a fixed percentage of the assets, which is valued annually. You get this income for a fixed period of years.

Summary

GRITs, GRATs and GRUTs are irrevocable trusts. Their purpose is to transfer assets to your heirs at a reduced gift tax value. You retain the right to receive income payments for a fixed period of years. At the end of the term, ownership of the assets shifts to your heirs.

Note:

Grantor Retained Trust – minimize estate taxes on financial gifts to family members. (this page)

Charitable Trusts – reduce taxable income of individuals, reduce estate taxes and preserve highly appreciated assets.