Life Insurance Trust

Why you need to leave tax free immediate cash for your heirs upon death…

There are important reasons to setup an insurance trust if your estate value exceeds $11,500,000 in this year 2020. The primary feature is that cash death benefits are free of estate taxes. This means you could, for example, leave an additional $3,000,000 without paying estate taxes.

Ownership of the life insurance policy is either you personally or the trust. Taxes are the principal issue. However, in either case death benefits still provide your heirs with cash when it’s most needed.

Your Three Priorities

Formulating a plan to provide immediate liquidity for the family upon death is your first priority. Each person has their own view of immortality. But you still need to prepare for heirs in case it doesn’t work out. This is the moment when liquid cash becomes important.

Immediate survivors experience conflicting emotions. And your trustee has urgent time constraints to make major decisions. Your family will need cash to pay for planned and unplanned expenses.

Calculating what amount of liquidity will be needed to administer your estate is your second priority. Soon after your death, the process of administration begins. This is the next challenge for your loved ones, your executor, your trustees. They’re responsible for paying bills, collecting debts, preparing distributions, making gifts and the final tax return. Is there enough cash to pay off margin accounts, property loans and other investment obligations?

Estate Taxes are your third priority. If you leave an estate exceeding the $11,500,00 lifetime exemption, heirs face estate tax obligations of up to 40% of the value of your estate. Using the previous $3,000,000 would see $1,200,000 tax obligation – paid in cash within 18 months or it begins to accrue interest. Without liquidity, heirs may need to obtain equity loans or quickly sell assets.

Immediate Cash, Administration, and Tax Liabilities

Premiums are your primary expense. Think of it like an option contract. The death event exercises the option. Cash is paid to close out the option.

Life Insurance Trust as the Owner?

When your gross estate exceeds $11,500,000 in the year 2020. Anything less, you can omit the trust instrument and just get the insurance.

Example:

Look at the numbers. If you have a $11,500,000 estate and your $3,000,000 life insurance policy is in your name, your taxable estate is $14,500,000.

- $3,000,000

- – $1,200,000 (estate tax 40%)

- = $1,800,000 net

Zero estate taxes if your life insurance policy is owned by a trust. Your heirs get the full $3.000,000 benefit.

The Importance of Two Policies If Married

If married and the collective estate exceeds $23,000,000, then consider two insurance policies. Each spouse is safer with their own policy for the benefit of alternative heirs.

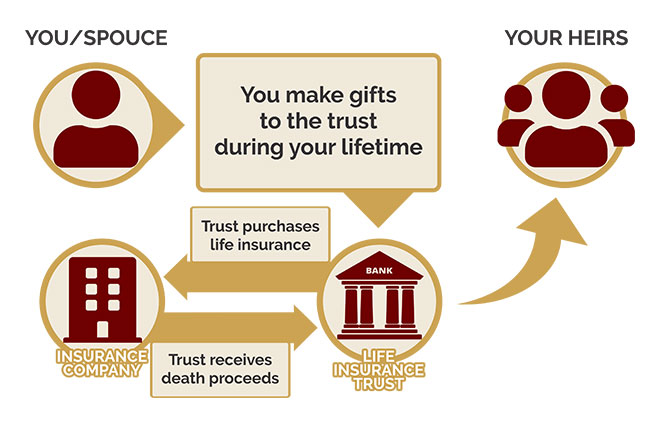

How Does It Work

You create an insurance trust. The trustee buys an insurance policy on your life. Upon death, cash benefits are paid to the trust. You cannot ‘undo’ or cancel because it’s an irrevocable trust. However, if the policy lapses due to nonpayment of premium it can ruin your plans.

This is a ‘single asset’ trust, nothing else. The trust gets an EIN and bank account to receive your gifts, pay premiums, receive the death benefit, and distribute proceeds to heirs.

Flexible Directives

Depending upon your needs and personal situation, you might have more than one insurance trust. What if you prefer to keep a beneficiary anonymous and separate from your other affairs? You can also dictate the terms of any trust payout, e.g., immediate disbursement for taxes, obligations paid, staggered income payments for a beneficiary, medical emergencies, funds for college education, gifts, etc. Or you can leave it all up to the discretion of your trustee.

An Important Note About Who Funds the Policy

The purpose of an insurance trust is to exclude the cash death benefit from your taxable estate. For this to be effective, the trust is the legal owner. If you are married in a community property state, it is imperative that you fund the trust with sole and separate property.

You can use the annual gift exclusion ($15,000 in 2020) to one individual (heir) given to the trust to pay premiums. If the premium is $30,000 annually, then two gifts for two individuals (heirs) can pay the premium. However, these gifts are “unrestricted.” This means beneficiaries have the right to receive and spend the $15,000 gift money. But practically speaking they leave it untouched for 30 days. Afterwards those funds pay the policy premium.

History

This mechanism to fund premiums with a tax-free gift is also known as a “Crummey Power.” It was first established in 1968 from a landmark IRS case. Sometimes it’s known as a Crummey Insurance Trust. In 1985 the Cristofani case arose when “contingent, successor beneficiaries” were named. The idea was to multiply annual tax-free gifts. The IRS challenged this expansion.

Setup & Selection of Trustees

You will incur professional fees to set up an insurance trust. The minimum people you need include a trustee, a life insurance representative, and accountant. You might also engage a tax attorney to do a review.

If you currently own a policy, it is possible to transfer ownership to the trust subject to the insurance company’s approval. However, if you die within three (3) years of transfer, the proceeds might be included in your estate.

The safest approach tax wise is to get a new policy. Yet sometimes a new policy is difficult because of recent medical issues.

Trustee selection requires careful consideration with respect to experience, integrity and knowledge of financial matters. They can earn fees. The trustee must remain vigilant so the policy remains in force. They must follow strict rules and communicate with the insurance company in a timely manner, and pay premiums on time.

Summary

If you’d like to leave heirs additional funds above the lifetime gift exemption then a life insurance trust is the solution. The death benefit provides liquidity when it’s most urgent.