Senator Roth from Delaware provided Americans with a tremendous gift in 1997. He sponsored a bill for a new type of retirement plan. It changed the way people earned, saved and invested. We know it as the ROTH IRA.

But there’s a problem with most companies who administer your retirement account. You can only buy their investment products.

So what if you want a classic car or artwork investment? Then you need a self-directed account.

Many people ask how ROTH is different than a regular IRA and other retirement plans. There are two distinctions…

- Traditional IRA contributions are pre-tax dollars. You pay taxes on withdrawls.

- ROTH IRA contributions are post-tax dollars. You withdraw any amount free of federal taxes.

Investment Opportunities

Maybe you want to invest in Canadian Maple Leaf, or a Collectible Motorcar. You might also invest in Artwork, Tapestries or Antique Furniture. Rather than just look at a brokerage account statement, you might prefer to enjoy an appreciating tangible investment.

One of the best strategies to boost your account value are options. Consider buying an option on real estate for $2,000 which is then resold for $50,000. This means that $48,000 can go into your account tax free.

Self-Directed IRAs allow you alternative investments such as real estate, promissory notes secured by a deed of trust, promissory notes secured by a mortgage, tax lien certificates, private companies, private placements, etc.

Special Custodians

These are the companies that administer your account. They are necessary because you cannot touch your pension funds. But you can choose the investments.

Most any commercial lending institution, mutual fund and stock brokerage will act as your custodian. However, they only allow you in house ‘approved’ investments. They block you from making outside investments.

You need a truly self-directed account custodian. Here are a few examples…

Equity Trust Company

Westlake OH

IRA Resources

La Jolla CA

Quest Trust Company

Houston TX

Investment Vehicle

For years investors have used LLCs to make their self-directed investments. But they have several drawbacks.

You obligate yourself to government bureaucrats. They will give you the privilege of operating and LLC in exchange for Secretary of State registration, franchise taxes, and resident agents. And since your LLC is online for anyone to see, you’re at risk for business identity theft.

Here’s one risk – your ROTH is the member and you are the manager. This might be too close of control.

The smart alternative is to use a Holding Trust. No state registration. No franchise taxes. No resident agent. It’s all quiet and private. permission required. Business identity theft is eliminated because the trust is unlisted.

Might an acquisition benefit by having an obscure buyer? This might work well at a major auction house to sandbag the competition.

This is one of the least-known uses of a Holding Trust – controlling your self-directed ROTH IRA.

Operational

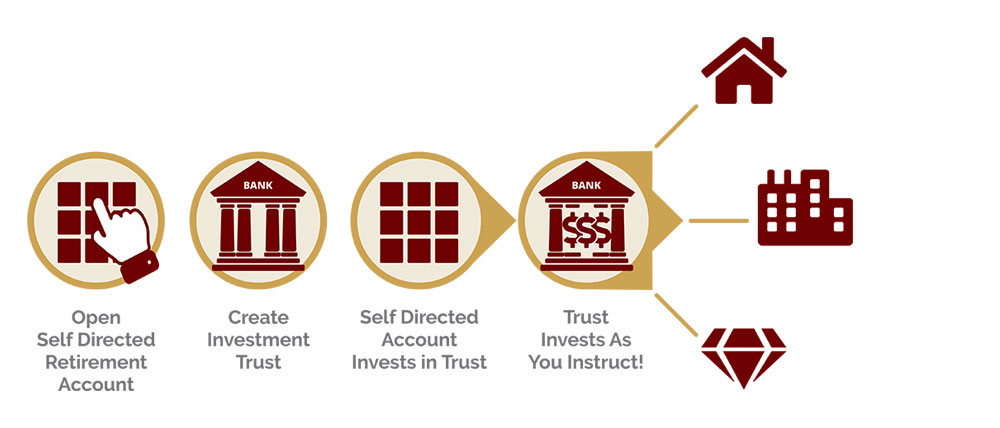

How you make this work is ‘direct’ your custodian to buy all the shares of your Holding Trust. Your trust opens a bank account and is funded by the custodian. The exchange is dollars for shares. Then your trustee makes investment transactions at your direction.

The main benefit of using the trust is avoiding the delay, paperwork and expense of going through your custodian every time you want to make an investment. You just write a check on the spot.

No relatives permitted to act at your trustee. An unrelated, trusted close friend is ok.

For our IRA we don’t use a business trust because it can earn active income. A Holding Trust is better since its activities are normally non-active or rather passive income from capital gains, interest, rents, options, royalties, etc.

However, if you want to invest in an ongoing business while avoiding active income – rather than have your ROTH Custodian directly invest in the business – use a trust to make the investment.

Some people have been known to have their friend trustee sign a bunch of blank checks. This might not be technically correct. Remember you can make the decisions, but never touch (comingle personal accounts) the money in any way otherwise jeopardize the account. You could lose all tax benefits back to day #1.

At the end of the year your Trustee sends an account statement to the custodian listing all gains/losses for tax reporting. However, you do not need to return any funds to the custodian, only notify them of your investment activities. Your custodian can provide reporting instructions.

Optional

You can also use a self-directed holding trust for Health Savings Accounts (HSA) and Qualified Pension Plans (401k).

Summary

In either case with a self-directed ROTH IRA – you can use an LLC or Business Trust. Again the difference is that your LLC is public information, incurs fees & taxes as well as regulatory requirements.

In contrast your Holding Trust is paperwork light, without any fees or tax and is totally anonymous.